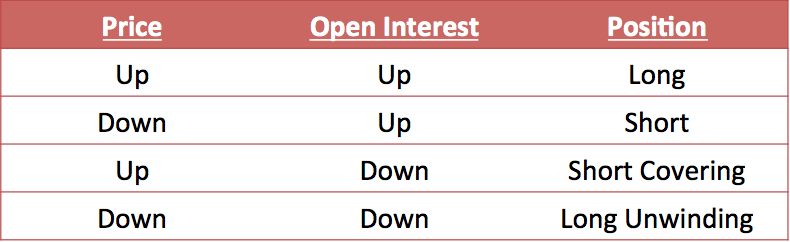

Содержание

However, if the sharp ratio is below CML you should sell your shares/assets. For an investor who underestimates or overestimates, this kind of calculation system is a systematic risk. On the other hand, SML determines both functioning and non-functioning portfolios. On the other hand, the Beta coefficient determines the risk factors of SML. The CML intercepts the vertical axis at point Rf, i.e., the risk-free rate.

It’s termed as a systematic risk since all the possible risks that could exist on their own are taken into account while computing this measure. Just as the CML gives us the rebound rates for a particular profile, SML serves the market risks and rebounds given time and exhibits rebounds from each share. Determination of risks in CML is the general divergence, whereas the determination of risks in SML is done by beta or systematic risk. CML provides reports that excellently merge risks and rebounds.

thoughts on “CML VS SML – Capital Market Line and Security Market Line| Finance”

This will always be a combination of the risk free security and the market portfolio. Hence, the CML will intersect the second axis at the risk free rate and go through the market portfolio. It is important to note that all portfolios on the CML offer a superior risk-reward profile to any portfolio on the efficient frontier.

The Capital Market Line is a graphical representation of all the portfolios that optimally combine risk and return. CML is a theoretical concept that gives optimal combinations of a risk-free asset and the market portfolio. The CML is superior to Efficient Frontier because it combines risky assets with risk-free assets.

In philosophy, profiles that rely on CML have excellence in terms of risks and rebound and give good results. The CAL arranges the slab of non-risky shares and dangerous shares for the dealers. The purpose of investors is to increase returns while increasing market risk. However, it very effectively represents the total risk-free return of all investment portfolios.

We’ve updated our privacy policy.

The cml vs sml is a line that is used to show the rates of return, which depends on risk-free rates of return and levels of risk for a specific portfolio. SML, which is also called a Characteristic Line, is a graphical representation of the market’s risk and return at a given time. One of the differences between CML and SML, is how the risk factors are measured.

Valuation Models: Apple’s Stock Analysis With CAPM – Investopedia

Valuation Models: Apple’s Stock Analysis With CAPM.

Posted: Sat, 25 Mar 2017 02:32:54 GMT [source]

Mean-variance analysis was pioneered by Harry Markowitz and James Tobin. The efficient frontier of optimal portfolios was identified by Markowitz in 1952, and James Tobin included the risk-free rate to modern portfolio theory in 1958. William Sharpe then developed the CAPM in the 1960s, and won a Nobel prize for his work in 1990, along with Markowitz and Merton Miller. In SML, the formula to calculate slope is (Rm – Rf), while the formula in CML is (Rm– Rf) / σm. The slope in SML tells the difference between the required rate of return and the risk-free rate.

Are CML and SML (Security Market Line) similar?

The above pages discussed some of the most widely used financial management concepts, such as CAPM, diversification, efficient portfolios, SML and CML. In this post I address one common question students have about the capital asset pricing model . Under the standard assumptions and in the presence of a risk free investment, the capital asset pricing model can be described using two equations. Low variance reluctant dealers will go for profiles with bigger CML and expect a big rebound and more risks.

If you want to avoid some of the troubles that may come your way, it is important for you to understand stocks, marketplace business, prices, and returns. To do this accurately and effectively, two key terms are CML and SML . These two lines can be found on any chart as they help track both profits from a company’s sales products along with their costs.

SML (Security Market Line)

The graphs of the Security Market Line define both efficient and non-efficient portfolios. Security Market Line measures the risk through beta, which helps to find the security’s risk contribution to the portfolio. SML defines both functioning and non-functioning portfolios, or we can say efficient and non-efficient portfolios.

- Capital Market Line represents the portfolios that accurately combine both risk and return.

- It is a theoretical concept that represents all the portfolios that optimally combine the risk-free rate of return and the market portfolio of risky assets.

- The portfolios on the CML optimize the risk and return relationship.

- Similarly, these two terms are very useful to those who enter the business world.

While standard deviation is the measure of risk for CML, Beta coefficient determines the risk factors of the SML. The CML measures the risk through standard deviation, or through a total risk factor. On the other hand, the SML measures the risk through beta, which helps to find the security’s risk contribution for the portfolio.

Drawbacks of CML

However, some people find it more convenient to refer to the CML for measuring the risk factors. In order to get comparable data for risk free rate of return, average rate of return in the market and beta value, the CAPM model assumes single-period horizon for all transactions. Typically, one year period is utilized for calculating all the inputs, although this period can be changed basis requirement. While calculating the returns, the expected return of the portfolio for CML is shown along the Y- axis. On the contrary, for SML, the return of the securities is shown along the Y-axis. The standard deviation of the portfolio is shown along the X-axis for CML, whereas, the Beta of security is shown along the X- axis for SML.

Stocks offer guaranteed returns, bonds offer higher potential returns.

In a broader sense, the SML shows the expected market returns at a given level of market risk for marketable security. The overall level of risk is measured by the beta of the security against the market level of risk. Basically, SML tells about the market risk in an investment or identifies a point beyond which an investor may run into risk. Or, we can say it tells the relation between the required rate of return of security as a function of the non-diversifiable risk . In common words, it determines the degree of your profit in the market as per your investment. CML primarily shows the trade-off between risk and return for functioning portfolios.

Thus the conclusion is, you purchase when the acute ratio is beyond CML, and you sell if the ratio is beneath CML. Capital Market Line shows the relationship between the expected return on efficient portfolio and their total risk. • The security market is the representation of the CAPM model in a graphical format.

Absence of https://1investing.in/-free asset − The CML concept is built on the principle of the existence of risk-free assets. In reality, there is hardly any asset that is a risk-free asset. SML considers only systematic risk, while CML considers both systematic and non-systematic risk.

While SML represents CAPM graphically, CML represent efficient portfolios and minimum variance portfolios graphically. Explain and graphically depict how security market line is different from Capital Market Line . Identify and discuss the importance of minimum variance portfolio? Why CAPM equation might be more relevant than other equations when calculation required rate of return. The efficient frontier comprises investment portfolios that offer the highest expected return for a specific level of risk.

Diferença entre CML e SML

As a result, they expect a handsome return on their wealth as per the capital market line exhibits graphically. In contrast, SML defines both efficient and non-efficient portfolios. Security Market Line shows the relationship between the required return on individual security as a function of systematic, non-diversifiable risk.

Hence, while all portfolios on the CML are efficient, the CML does not contain all efficient portfolios. A beta value that’s greater than one represents a risk level greater than the market average, and a beta value of less than one represents a risk level that is less than the market average. The beta of a security is a measure of itssystematic risk, which cannot be eliminated by diversification.